Single-family home prices have dramatically outstripped the ability for the average worker to buy homes in New Hampshire.

Across New Hampshire, a lower inventory of single-family homes, rising sale prices and fewer days on the market point to a growing trend: a workforce housing shortage.

“I don’t think there’s any community in the state that doesn’t have some issues in terms of ensuring that there is adequate housing and the type of housing that workers are seeking,” said Bob Quinn, vice president of government affairs for the New Hampshire Association of Realtors.

Local zoning regulations, higher building costs and labor shortages in the construction industry are a few factors affecting the inventory of workforce housing. This shortage affects areas across the state.

The statewide monthly inventory of single-family homes for sale has dropped by about 55 percent since 2014, according to NHAR monthly indicators. Fifteen years ago the state averaged about 11,700 homes for sale each month. Last year, the monthly average was about 5,200.

New Homes Are Higher-End

In some New Hampshire counties, the houses for sale are not affordable.

A single-family home in New Hampshire is considered affordable at $300,000, according to the New Hampshire Housing Finance Authority. For newly constructed homes, the median sale price in 2018 was $374,300, almost 19 percent higher than in 2014, according to the NHHFA. For existing homes sold in 2018, the median price was $250,000.

Looking at the overall numbers for single-family homes, the statewide median sale price was $265,000, up 22 percent since 2014, according to The Warren Group.

Single-family homes are also selling more quickly, another sign of a workforce housing shortage. Single-family homes for sale in the past two years spent fewer days on the market than at any other time during the past 20 years: 68 days in 2017 and 61 days in 2018, according to the NHAR. That’s about a month shorter than in 2014 and two months shorter than in 2011 and 2012.

Every county saw single-family homes spend fewer days on the market in 2017 and 2018. In most counties, the number of days on the market has dropped year after year since 2012, according to the NHAR.

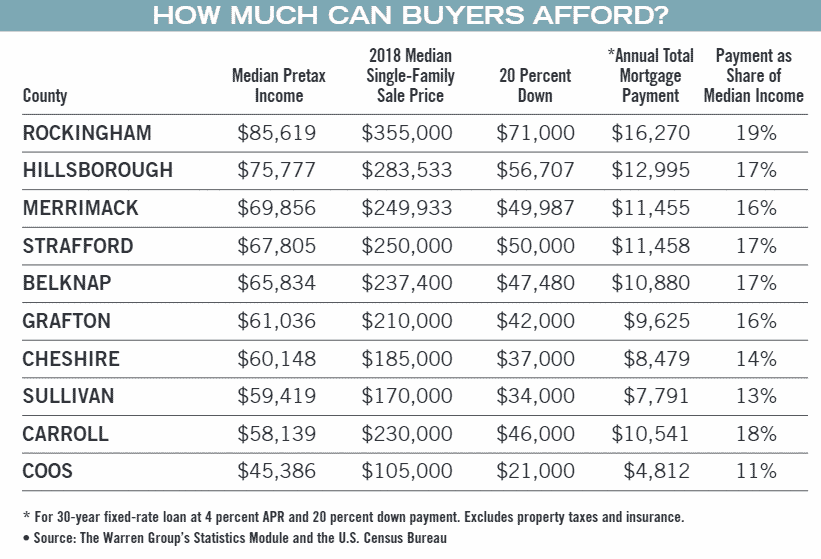

In Rockingham County, the median sale price was $355,000 in 2018, a 30 percent increase since 2014, according to The Warren Group, publisher of Registry Review, while the median income has only gone up 7.3 percent according to the U.S. Census Bureau. A family making the median household income in the county – $85,619, according Census figures – buying a median-price home today would wind up paying just over 19 percent of their pretax income on a conventional, 30-year, fixed-rate mortgage with a 20 percent down payment and 4 percent interest rate, the current national average according to Freddie Mac.

The story is similar in Hillsborough County, with a median home sale price of $285,000 last year, up from $228,000 in 2014, and a median income in 2017 of $75,777. A similar mortgage on the median-price home would cost a family making median income nearly 17 percent of their pretax income, without taking local property taxes into account, which can run over $5,000 per year in some communities.

The trend doesn’t seem to be slowing. While the median sale price in most counties remains below $300,000, prices continue to rise.

Merrimack County, for example, has seen its median sale price rise by almost 25 percent since 2014, to $249,933 in 2018. Even Coos County – median household income $45,386 – has started to see changes. The median sale price rose 31 percent between 2017 and 2018, to $105,000.

Regulations, Labor Costs Drive Trend

Some causes of the workforce housing shortage are not unique to New Hampshire, said Dean Christon, CEO and executive director of the NHHFA. A labor shortage in the construction industry and rising costs for materials to build new homes have affected development across the U.S., Christon said, adding that in recent years, construction costs have risen faster than incomes.

Zoning regulations are also a contributing factor. While policies designed to control density, scale and over-development affect communities across the country, Christon said New Hampshire “has it a little bit worse” compared to other places.

“Now we find ourselves in a scenario where, for a variety of reasons, there’s not a lot of housing development going on,” Christon said. “Those regulatory policies in many cases further limit, further impede what development might otherwise occur.”

“If you’re going to have small businesses, if you’re going to have service workers, they’re going to have to live some place. Continually driving the costs of rental properties and single-family homes higher and higher is going to have real consequences on the economy.”

— Bob Quinn, vice president of government affairs, New Hampshire Association of Realtors

While the demand for affordable, single-family homes is most obvious in areas from Concord south and in the Upper Valley, other parts of the state feel the effects as well.

Andrew Smith, with Peabody and Smith Realty in Franconia, said local zoning requirements have affected workforce housing inventory in central and northern New Hampshire, making affordable projects difficult to build. The cost of construction is even higher up north, Smith added, and many developers find building high-end homes to be more profitable.

Student Debt Hurts Younger Buyers

Workers encounter other challenges when seeking affordable housing. Smith said student debt has prevented potential borrowers from qualifying for the mortgages needed to afford median sale prices. The NHHFA reports that New Hampshire has the highest percentage of students graduating with debt in the U.S. and the fourth highest amount of debt per student.

Younger workers are also competing for the same inventory with older residents looking to downsize, Christon said. Older residents have more equity and can often make higher offers.

Condominiums face a shortage similar to single-family homes. Rental units are experiencing low vacancy rates as well, according to the NHHFA, further limiting housing options.

The workforce housing shortage could have long-term consequences.

“If you’re going to have small businesses, if you’re going to have service workers, they’re going to have to live some place,” said the NHAR’s Quinn. “Continually driving the costs of rental properties and single-family homes higher and higher is going to have real consequences on the economy.”